|

|

|

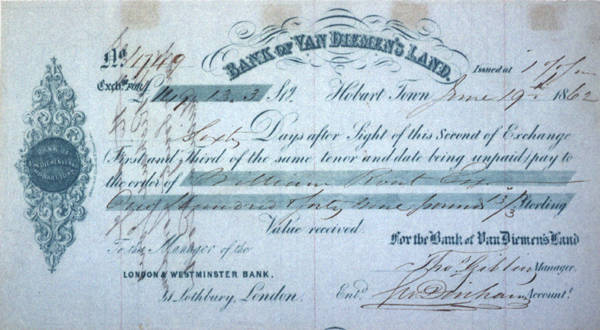

Banking and Finance The absence of a monetary constitution when Australia was settled in 1788 created the conditions for a century of free banking. Banking companies proliferated in this unregulated environment and Van Diemen's Land was unexceptional. Fifteen banks operated in the first fifty years of Van Diemen's Land's existence, out of an Australian total of 51. They were generally of a limited size and operated on a small scale. Consequently many failed, while others merged with larger banking companies, particularly those with branch banking structures. Banks were set up either as regular commercial institutions, such as the Bank of Van Diemen's Land (1823), or in philanthropical vein to encourage the lower classes to save their money. Sometimes these aims were combined. When the Derwent Bank was established in 1829, attached to it was the Convict Savings Bank, an attempt to encourage convicts to improve their miserable status. The major banks of this type, both aiming at all the'lower classes', were the Launceston (1835) and Hobart (1845) Savings Banks.

The Bank of Van Diemen's Land lasted seventy years before failing in the 1891 Depression, as mineral prices crashed and certain key mining ventures reneged on loans. This major banking event was preceded by other bank failures: the Tasmania Bank (182629); the Derwent Bank (182749); the General Savings Bank (183138); the Archer Gillies Company (184043) and the Colonial Bank (184043). Other smaller banking companies were merged: the Cornwall Bank (1828) was absorbed by the Bank of Australasia in 1835; the Convict Savings Bank (attached to the Derwent Bank) and the Tamar Bank (1834) were absorbed by the Union Bank in 1851 and 1838 respectively, while the Commercial Bank of Tasmania was absorbed by the ESA Bank in 1921. The Tasmanian banking institutions surviving well into the twentieth century were two trustee savings banks, namely the Launceston and Hobart Savings Banks, plus the Agricultural Bank of Tasmania (1840) which specialised in rural finance. Attempts to merge the two trustee savings banks into a single state Bank of Tasmania in the mid-1980s failed on parochial grounds, although the Tasmania Bank was created through the merger of the Launceston Bank for Savings and the Perpetual Executors Building Society. The Hobart Savings Bank continued its separate existence until Tasmania Bank entered a crisis phase in 1989 as a result of poor lending strategies. The Trust Bank of Tasmania rose from the ashes of the Tasmania Bank initiated by a significant injection of state government funds and the inclusion of the Hobart Savings Bank. The new Trust Bank retained the trustee structure of its predecessors. However, the Trust Bank could not sustain a competitive position in the Australian capital market, given its smallness, and so its assets were purchased by the Commonwealth Bank of Australia in 1998. Tasmania's flirtation with state banking had finally passed and the island's financial needs were serviced by the four major national banking chains, two national insurance groups, one building society, two major credit unions and a plethora of accountants and financial advisors. A recent addition to Tasmania's financial market was the Bendigo Bank (from 2000), which introduced community banking to Tasmania, resurrecting some of the original ideals of the savings banks. The shadows of financial deprivation have always hung over the island economy, a fact which is evident in its colonial beginnings. The Commissariat Store was the only institution providing a treasury or banking function for Van Diemen's Land in its prison farm existence. The colony's wool and wheat exports generated a growth spurt over the period 1810 to 1830 which was financed by a variegated collection of currencies. These included the Spanish and South American dollars, rupees, sterling and US dollars. In spite of New South Wales legislation to establish a dollar standard in 1822, followed by a sterling standard a few years later, the variegated collection of currencies acceptable for exchange media in the Tasmanian economy continued for several years. This is largely explained by the shortage of sterling circulating in Van Diemen's Land. The island economy experienced a shortage of financial capital throughout its history and this has undoubtedly impeded its economic development. Tasmania's golden era of capital accumulation occurred in the hydro-electric building era of the 1950s and 1960s, when both public and private expenditure of a capital nature was at its peak and ran at levels above the Australian average. In the aftermath of the Gordon-below-Franklin dam fiasco, business investment in particular dried up in the absence of major projects on the island. In relation to public finances, Tasmania's development has been impeded by the narrowness of its tax base. The effects of this restriction were self-evident through the Great Depression, and the financial hardships of this episode were most strongly felt in Tasmania and South Australia. The Commonwealth Grants Commission was established in 1933 to deliver to the smaller Australian states a disproportionate share of the Commonwealth income tax revenues to compensate them for their financial disabilities. The principle of fiscal equalisation delivered to the smaller states the same range of public services as those enjoyed by the standard states of New South Wales and Victoria. The same principles apply to the distribution of the proceeds of the Goods and Services Tax (GST) introduced in 2001. This consumption tax is collected by the federal government and is distributed through the Commonwealth Grants Commission to individual states and territories. For the first time the Australian regions are enjoying the proceeds of a genuine growth tax. Further reading: S Butlin, Foundations of the Australian monetary system, 17881851, Sydney, 1968. Bruce Felmingham |

Copyright 2006, Centre for Tasmanian Historical Studies |