In this topic you will revise the following

Lesson 1 - Fractions, Decimals and Percentages

Lesson 2 - Percentage Mark Ups and Mark Down

About This Lesson

Image: Skillswise

These topics were introduced in Module 1.

is the same as 0.75 is the same as 75%

In this lesson you will look at the three ways of representing fractions and convert between them.

Fractions are numbers expressed like this

with a numerator, on top to tell you how many parts there are and a denominator on the bottom to tell you how big the parts are.

In this case there are 3 parts and each is one quarter of a unit.

Decimals are a different way of expressing a fraction by showing it as part of one unit using place value to show the size of the numbers.

Percentages are another different way of expressing a fraction by making the denominator always equal to 100

and is written 75%

Basis Points

Basis Points is a term you will come across, especially when looking at interest rates or share price movements. To quote from the Reserve Bank of Australia Glossary:

| "A basis point is |

It is used because some changes can be very small and would more difficult to understand if written as percentages.

Test Yourself

This interactive worksheet and self test will help to check your skills and fill in any gaps.

Learn More

Look at BBC Skillwise for fractions, percentages and comparing between the two. Follow the links below for the lessons.

Maths is Fun - Decimals Fractions and Percentages

Khan Academy Series - Introduction to Percentages there are 13 video lessons and 4 practice exercises.

About This Lesson

In this lesson you will revise the following concepts and practice them.

Mark Up

When a product is bought at a wholesale price and sold at a retail price, the difference is called a Mark Up. For example a fashion shop might have a normal mark up of 60% meaning that if it buys a dress for $50 from the manufacturer it will increase the price by 60% before selling it

$50 x 60% = $30

So the mark up is $30 and the selling price is $90

Mark Down

When a product hasn't sold well or it becomes out of season, the retailer may mark down the price. This is the exact opposite of marking up.

25% off everything

$90 x 25% = $22.50

So the mark down is $22.50 and the new selling price is $67.50

Discount

This is another way of describing a markdown. Prices may be discounted because you are a major customer, buy large quantities or are a member of a club for example.

Test Yourself

This interactive worksheet and self-test will help to check your skills and fill in any gaps

Note: this is from the UK and is in pounds

Learn More

Image : Maths is Fun

Khan Academy Series and Self-test - Percentage Problems Examples

In this topic you will revise the following

Lesson 1 - Simple and Compound Interest

Lesson 2 - Inflation and Effective Interest Rates

About This Lesson

Interest

Simple Interest

Simple interest is the absolute interest (I) that is paid on the funds that are borrowed, lent or invested.

The sum loaned or advanced, is often referred to as the principal (P).

The time (t) until the principal is returned is known as the term usually in years.

The rate of interest (r), is the interest usually per annum as a percentage.

So for Principal = P, term = t, Interest = r

Then the Interest: I = P·r·t

The value (S) at maturity is: S = P + I

S = P + P·r·t

S = P(1 + r·t)

Example

An investment of $100,000 in a project that took five years and yielded $30,000 profit would be a simple interest of $6,000 per year or 6%

Simple interest is so called because it ignores the compounding effect.

Money Chimp - Simple Interest Calculator

Image: Moneychimp

Compound Interest

Most interest is actually compound interest, which means that interest paid is added immediately to the principal as it is paid. This interest is then part of the principal the next time interest is calculated.

Interest is often quoted annually but the payment of interest can be monthly or even daily which creates even greater growth in the principal.

Where the Principal = P, the term at which interest is paid = t, the rate of interest = r and the accumulated value at the maturity date = S

Note: that t = 1, i.e. interest is paid each year

Year 1: Total value after one year

S1 = P + P·r = P(1 + r)

by taking the common factor P

Year 2: Total value after two years

S2= P(1 + r) + r·P(1 + r)

by taking the common factor P(1+r)

= P(1 + r) (1 + r)

= P(1+r)2

Year 3: Total value after three years

S3= P(1+r)2 + r.P(1+r)2

by taking the common factor P(1+r)2

= P(1+r)2 (1+r)

= P(1+r)3

And so on

After t years: St= P(1+r)t This is called the Compound Interest Formula.

Compounding more frequently

In many cases the interest is paid monthly in which case the formula becomes one twelfth of the interest rate paid every month.

St= P(1+r/12)12t

Or generally if m is the number of payments in the year:

St= P(1+r/m)mt

Money Chimp - Compound Interest Financial CalculatorIncludes periods less than 12 months

There are plenty of opportunities to revise this in the resources below.

Learn More

Study Maths - resource on simple and compound interest, follow the links below;

Introduction to Compound and Simple Interest - This resource is from the UK so is in pounds

Khan Series - Interest and Debt

You Tube Tutorial - Watch the Compound Interest tutorial below;

About This Lesson

Inflation

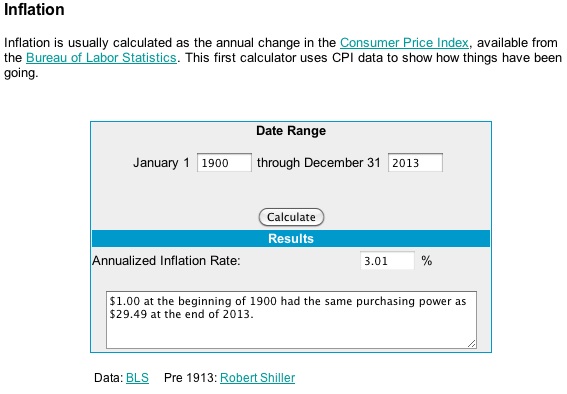

The cost of goods and services tends to rise over time though there are exceptions to this. This rise is called inflation and is measured by using standard data such as the Consumer Price Index which is calculated by the Australian Bureau of Statistics. When overall costs fall over a period, that is called deflation.

This calculator allows you to find the average annual inflation rate in the USA

The overall concept of inflation is explained in this tutorial

Nominal and Effective Rates of Interest

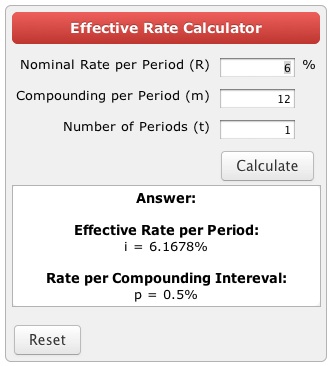

If you invest money in a bank account to earn interest and the bank says the interest rate is 6% per annum, this is called the nominal rate of interest.

You also need to know how often the interest is compounded in order to calculate how much interest you will earn.

If interest is compounded at the end of each year then the effective rate of interest is also 6% but if the interest is compounded every month, the effective rate is 6.17% which is (1+0.005)12 because 0.5% interest is applied 12 times during the year.

This calculation is shown in this calculator.

Learn More

Khan Academy Series - Inflation

TeachMeFinance - Nominal and Effective Rates of Interest

In this topic you will revise the following

Lesson 1 - Depreciation

Lesson 2 - Break Even Point

About This Lesson

Some assets such as vehicles, computing equipment, tools and machinery lose value over time. This loss of value is called depreciation and needs to be considered in the accounts of a business. There are sometimes tax allowances for depreciation and agreed ways of calculating them.

If an asset is relatively cheap, say $1000 or less, it may be considered as a single expense rather than a depreciating asset. For specific details you would need to refer to current tax arrangements.

There are two common ways of calculating depreciation:

These are the terms used by the Australian Tax Office but there are other names for the same methods.

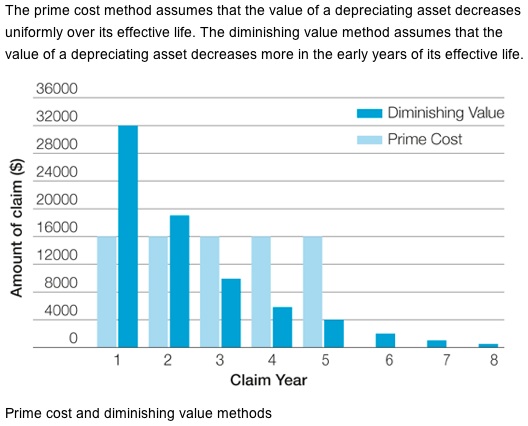

Prime Cost Method

Also known as Straight Line Depreciation

Assumes that the asset loses value equally over its lifetime. For example a $100,000 machine that lasts for 10 years and is then worthless would be depreciated at $10,000 per year.

Diminishing Value Method

Also referred to as Reducing Balance Depreciation and Declining Balance Method.

Assumes that the asset loses more value in the first years than later years and so the depreciation calculated per year is always less than the year before until the asset is sold or has no value.

This chart from The Australian Tax Office compares the two methods for an asset purchased for $100,000. If you click on the chart, you will be taken to a detailed explanation and example at the ATO.

Image: https://www.ato.gov.au/Business/Deductions-for-business/Capital-allowances-and-depreciating-assets/Uniform-capital-allowances/Prime-cost-and-diminishing-value-methods/

Test Yourself

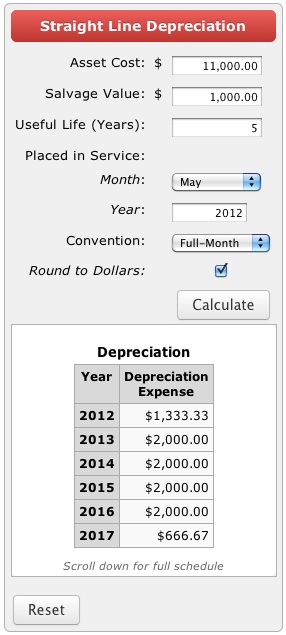

Prime Cost Method

Use the link to the calculator below to explore some examples of Prime Cost (Straight Line) Depreciation. Note that in this example the financial year is January to December so the first year has 8 months of use and the last year is 4 months of use.

Image: www.calculatorsoup.com/calculators/financial/depreciation-straight-line.php

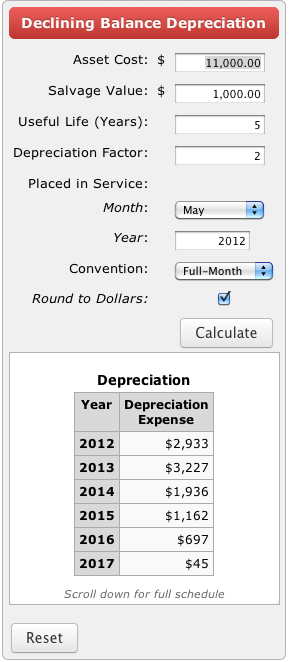

Diminishing Value Method

Use the link to the calculator below to explore some examples of Diminishing Value (Declining Balance) Depreciation. The example shown is for the same asset as above showing the difference between the two methods.

Image: www.calculatorsoup.com/calculators/financial/depreciation-declining-balance.php

Learn More

Watch the following videos

You Tube - Prime Cost Method Explained

About This Lesson

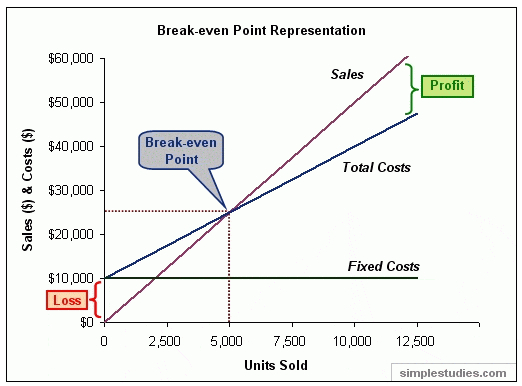

A business that sells a product has fixed costs such as rent, insurance and administration costs that stay the same no matter how much product they make or sell (within a reasonable range). There are also Unit Costs, which depend on the amount of product produced and would include raw materials, energy, packing and freight.

The break even point is the number of items that you need to make and sell to just cover all your fixed and variable costs.

This can be shown graphically.

In this example a company has fixed costs of $10,000 and makes a valve for $3 per unit that sells for $5 per unit.

Image: http://.simplestudies.com/accounting-cost-volume-profit-analysis.html/page/8

You can read about this example at

The Queensland Government has a web site to help business and industry and it includes a good guide to break even point calculation.

In this topic you will revise the following

Lesson 1 - Present and Future Value

Lesson 2 - Annuities

Lesson 3 - Amortisation

About This Lesson

If a customer offered to pay you $100 today or $110 in a year with no risk. Which is the better offer.

The $100 is the present value and the $110 is the future value. These are important concepts in finance.

The answer depends on the interest rate that you could obtain if you invested the $100 for 1 year and the frequency of compounding. This is just an application of the compound interest formula.

You need to know the present value (P) that will yield a certain future value (S) at a maturity date if interest is allowed to compound annually. This is found by using the present value (PV) formula.

S= P(1+r)t

Thus: P = S/(1+r)t

We are effectively stating that the present value (P or PV) of the maturity or future value (S) is less than the maturity value (S) because interest is compounded over a period of time.

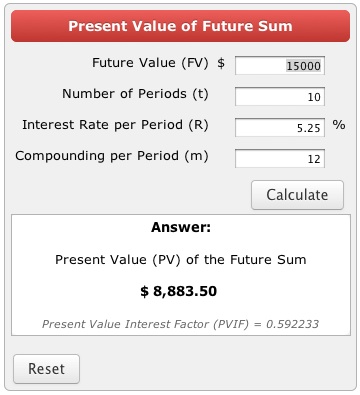

Test Yourself

This Present Value Calculator allows you to calculate the present value of a future sum.

Enter some different scenarios into this to test your understanding of this concept.

Image: www.calculatorsoup.com/calculators/financial/present-value-investment-calculator.php

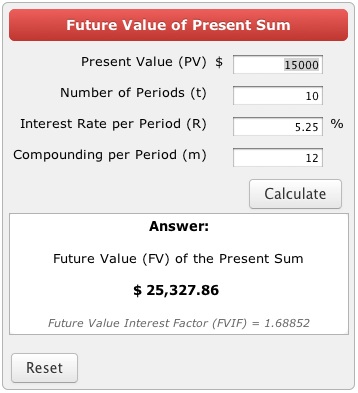

Future Value is exactly the same concept but the present value is known and the future value is calculated

Enter some different scenarios into this Future Value Calculator to test your understanding of this concept.

Learn More

Khan Academy Series - Present and Future Value

About This Lesson

According to Australian Security & Investments Commission (ASIC)" An annuity pays you a guaranteed income for a defined period of time. You can choose how long you want the payments to last e.g. a lifetime or a fixed number of years. This option gives you peace of mind that you will receive a fixed income no matter what happens."

When you purchase an annuity, you are basically giving a lump sum to a financial organisation and they guarantee you an agreed annual amount for an agreed number of years or until you die.

It can also include a form of insurance and so involves actuarial calculations as well as compound interest calculations because no one knows how long you will live.

For a detailed explanation see:

ASIC -

Perpetuities

If an annuity is set up to pay out forever, which means that the capital remains untouched and only the interest is paid out, then it is calla a Perpetuity.

About This Lesson

Amortisation

The term Amortisation has two different uses. One refers to the way a loan repayment is calculated and one refers to the way an asset is written off and is similar to depreciation.

Amortisation of a Loan

Amortisation refers to the way a loan repayment is calculated so that the interest and capital are repaid within the agreed time. Typically you would pay the same repayment amount every month but in the early stages most of this would be an interest payment with only a little of the capital (principal) paid off.

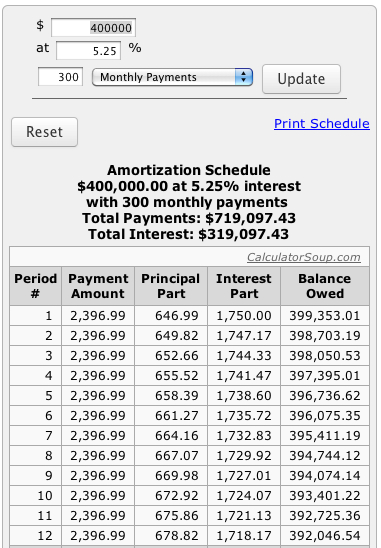

The example below shows the first year of a 25 loan for $400,000 at 5.25%. The monthly payment is $2396.99 but in the first month only 649.99 comes off the capital.

Image: www.calculatorsoup.com/calculators/financial/amortization-schedule-calculator.php

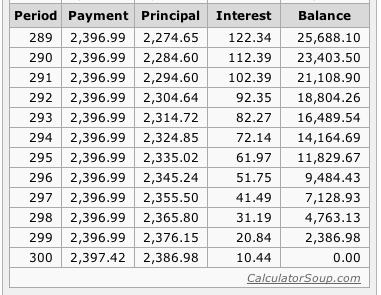

This table shows the last year of the same loan with the same monthly repayment but now most of this is capital (principal) not interest.

This example of amortisation illustrates why it can be sensible to try and pay a little bit extra in repayments in the early years of a loan and why it is important to try to avoid missing payments or going into arrears. The compounding effect on large numbers for long periods is very significant

Test Yourself

Use the calculator linked below to try some typical loans such as a loan to buy a new car or a mortgage on a property to check your understanding of amortisation.

Amortisation of an Asset

This alternative meaning for amortisation as a form of depreciation is explained in the following video

Money Week on You Tube - Accounting Jargon - Amortisation and Depreciation